May Maintenance: 10 Essential Home Maintenance and Hurricane Preparedness Tips for Florida Homeowners

Looking for referral, we've go you covered. Click the button below to be redirected to a list of companies that are our referral partners.  Are you ready to take the exciting leap into homeownership in the sunshine state of Florida? Congratulations on this significant milestone! As you embark on this journey, it's crucial to consider all aspects of homeownership, including the often overlooked but immensely important component of homeowners insurance.

At Anderson Agency Insurance, we understand the unique needs and challenges faced by first-time homebuyers in Florida. As a locally owned insurance agency, we're dedicated to providing personalized guidance and support to help you navigate the complexities of securing the right homeowners insurance policy for your new home. Why is homeowners' insurance so essential for first-time homebuyers in Florida, you ask? Let's delve into the key reasons:

Don't wait until it's too late to protect your new home and investment. Contact us today to learn more about the importance of homeowners insurance for first-time homebuyers in Florida and let us help you find the perfect insurance solution for your needs. Your dream home deserves the best protection, and we're here to make it happen.  A lot has changed in the time since Gerald Ford was president and Steve Jobs and Steve Wozniak founded Apple. But here’s something that hasn’t changed much: the pace at which car insurance rates are rising. Car insurance rates are up almost 21% for the 12 months ended in February, according to new Consumer Price Index data released Tuesday. The last time car insurance rates rose that much on an annual basiswas 1976, not counting January, which saw the same annual rate increases. The rise in car insurance rates alone contributed half a percentage point to the overall 3.2% inflation rate last month. It represents one of many obstacles standing in the way of the Federal Reserve’s 2% inflation goal and continues to be a pain point for Americans struggling with some of the highest prices in decades. A confluence of factors is behind the trend. Rising car repair costsThe cost to repair a car is up 6.7% for the year, according to CPI data. That’s a much slower rate compared to recent years. But it’s still much more expensive compared to before the pandemic, said Tim Zawacki, principal research analyst at S&P Global Market Intelligence. Contributing to the rising cost of repairing a car are more expensive auto parts and wage increases for car mechanics due to labor shortages, Zawacki told CNN. More severe and frequent car accidentsThe number of traffic deaths in the U.S. was up by around 7,000 in 2022, to 42,795, compared to before the pandemic, according to the National Highway Traffic Safety Administration’s latest estimates. That has led to an increase in claims that is well above historical averages because of their severity, according to LexisNexis Risk Solutions data. Their data indicates that insurers booked losses on 27% of collision claims in 2022. That’s three percentage points higher than 2021. LexisNexis also attributes that rise to riskier driving behaviors such as speeding, texting behind the wheel and driving under the influence of either drugs or alcohol. Beyond the repair costs associated with more severe car damage, they also “tend to lead to a higher share of claims with attorney representation, which usually ends up being more costly for insurers,” said Zawacki. Not all states have it quite as bad There’s a lot of variation from state to state regarding the car insurance rate increases that drivers are facing. That’s partially because auto insurers price their plans based on the losses they’re incurring on a state-by-state basis, Robert Passmore, vice president for personal lines at American Property Casualty Insurance Association, a trade group representing insurers, previously told CNN. Nevada drivers saw the highest jump — an increase of 38% — in car insurance rates across all states besides Wyoming from January 2023 to February of this year, according to data S&P shared with CNN. (Wyoming wasn’t included because S&P couldn’t collect data from the state.) The minimum required coverage policy that drivers in the Silver State have costs the most across all states, according to Bankrate data as of last month. Meanwhile, drivers in North Carolina saw the smallest bump in car insurance rates, up just 5.5% over that same timeframe. That’s partially due to the state’s unique format that includes a rate bureau that submits filings on behalf of the entire industry. That bureau settled on a 4.5% average statewide increase for 2023 and another 4.5% increase in 2024. “We do expect trends to moderate on a national basis over the course of the year, particularly in the second half of 2024,” Zawacki said. “But that doesn’t mean drivers in some markets won’t continue to see rate increases.” Although we do not have control over what is going on in the auto insurance market, we can ensure that you are getting the best coverage for your needs. If you haven's spoken to your insurance agent in the last 3-6 months, give us a call! We can help you with your insurance needs!

For an auto: The VIN, required by law, is a coded description of all the car's details. It appears in many places on the vehicle and in the documents--sales docs, registration, and insurance policy. If damage or a total loss occurs, the insurer and car owner have a detailed record of what was insured.

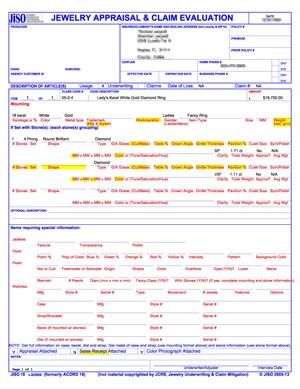

For jewelry: No VIN. Insurers must rely on appraisals and lab reports for detailed descriptions of gems and jewelry. Appraisals are crucial! If an auto VIN looked like the one pictured above, you'd be very suspicious, wondering what info was being concealed. At JIBNA we sometimes see appraisals that make us think of such a butchered VIN—jewelry appraisals with "holes" where there should be information. ACORD/JISO 18 is a tool we use to inform the agent and the insured when an appraisal has "holes" where important information should be given. We enter on the form all information given on the appraisal submitted, then our system highlights important details that are missing. Complete details allow JIBNA to appropriately insure the item and, if a loss occurs, to supply an accurate replacement. Yes, there are many insurers who do not require the details that JIBNA does. In fact, most insurers don't even read the appraisal. They just check that it has a date and a valuation. But once a loss occurs, perhaps years later, descriptive details can be hard to retrieve. Lack of important details means the insurer has to guess, and the replacement may not be like the original jewelry the insured so carefully chose. Why leave it up to guesswork later, when the appraiser can—and should—supply all the details upfront? If you receive such a highlighted form from JIBNA, discuss it with the insured. Explain how a detailed appraisal is in their interest, and they should insist on one. They can show their appraiser the highlighted form 18 supplied by the insurer and ask the appraiser to fill in the missing info. ACORD/JISO 18, the Jewelry Appraisal & Claim Evaluation form, is available free of charge from the Jewelry Insurance Standards Organization, www.jiso.org Interested in exploring a jewelry policy or any other insurance policy? We can help. Click the button below to submit a new policy/current policy review and a member of our team will be in contact with you.  The Allstate Corporation's ALL shares have advanced 29.1% in the past six months compared with the industry’s 5.3% growth. The Zacks Finance sector and the S&P 500 Composite Index rose 9.6% and 7%, respectively, in the same time frame. With a market capitalization of $37.6 billion, the average volume of shares traded in the last three months was 1.6 million. Rate hikes, the buyout of National General, an improved expense ratio in the Property-Liability unit, a well-performing Protection Services business and a solid financial position continue to drive Allstate’s performance. The property and casualty (P&C) insurer, currently carrying a Zacks Rank #3 (Hold), has a sound surprise history of beating on earnings in three of the trailing four quarters and missing the mark once, delivering an average surprise of 31.50%. Can ALL Retain the Momentum? The Zacks Consensus Estimate for Allstate’s 2024 earnings is pegged at $12.38 per share. The consensus mark for 2023 earnings is pinned at a loss of $1.89 per share. The consensus estimate for 2024 revenues is pegged at $61.8 billion, implying 7.6% growth from the 2023 estimate. The company's earnings witnessed three upward estimate revisions for 2024 in the past 60 days against two in the opposite direction. The top line of Allstate continues to benefit on the back of continually rising P&C insurance premiums and a diversified product suite. P&C insurance premiums improved 10.2% year over year in the first nine months of 2023. Continued rate increases are implemented to counter inflationary headwinds on loss costs, thereby acting as a roadblock to the profits of ALL’s auto insurance business. Allstate pursues acquisitions to enhance capabilities and expand its nationwide presence. The acquisition of National General in 2021 continues to reap benefits for the premiums of the Property-Liability segment and the trend is expected to sustain in the days ahead. Strong contribution from the Protection Services unit of ALL results from a growing product suite and international growth in Allstate Protection Plans. The insurer undertakes technology investments to solidify its position as a cost-effective digital insurer. Cost-cutting initiatives bring about improvement in underwriting results and the expense ratio of the Property-Liability unit. In the first nine months of 2023, the expense ratio improved 230 basis points year over year to 20.9%. Allstate divests underperforming businesses and thereby, redirects capital to boost presence in the personal property-liability market and expand protection solutions. A solid financial stand remains an added advantage for Allstate, substantiated by its growing cash reserves and adequate cash-generating abilities. Cash balance advanced 16.8% from the 2022-end level as of Sep 30, 2023. The financial strength imparts ALL to return capital to shareholders. In February 2023, management approved a 4.7% increase in the quarterly dividend. Allstate boasts an impressive VGM Score of A. VGM Score helps identify stocks with the most attractive value, the best growth and the most promising momentum. Original Story can be found: Allstate (ALL) Up 29% in 6 Months: What's Ahead for Investors? (yahoo.com) If you are a current Allstate customer and concerned about the rising prices we can help. By clicking the button below, our team can review your current policy and shop for one that better serves your needs. Plus, as a locally owned and operated business, we take pride in offering competitive rates and personalized service that you won't find with larger corporations. When you choose us, you're not just a policyholder - you're part of our community.

Allstate and State Farm, both based in Illinois, are said to be raising their homeowners' insurance rates in the state by double digits. Citing the insurance giants’ respective state filings, a Chicago Tribune report said Allstate’s 12.7% hike is being rolled out this week, while State Farm’s 12.3% increase will take effect on different dates – March 15 for new business; May 15, renewals. In terms of dollar amounts, Allstate’s adjustment will mean an additional $237 per year on top of the average annual premium; for State Farm, around $138. It was noted that, across the country, the cost of home insurance has gone up by 23% since January last year. “Estimated January catastrophe losses of $325 million were primarily driven by two events that comprised approximately 80% of the losses, partially offset by favorable reserve re-estimates for prior events.” In terms of auto insurance rates, Allstate plans to pursue rate increases in 10 states after implementing hikes in California, New York, and New Jersey last December. Allstate CEO Tom Wilson told the Tribune: “We still lost money on auto insurance last year. So, it wasn’t that we were raising the prices and going to the bank.” Original Article can be found here: Allstate, State Farm raising rates by double digits | Insurance Business America (insurancebusinessmag.com) At Anderson Agency Insurance, our role is to educate people about what is going on in the insurance industry. Staying in the know is one was we can help you make informed decisions about your insurance!

If we can help in any way please do not hesitate to reach out to our team by clicking the button below.  WEST PALM BEACH, Fla. — Two insurance companies have filed requests for rate hikes over 50% with the Florida Office of Insurance Regulation (OIR). Castle Key Insurance is seeking a 53.5% increase and Amica Mutual Insurance is seeking 54.1%. Both companies are seeking increases on specialized policies such as condos and second vacation homes. OIR has scheduled hearings next week on the requests, which is an automatic process on any hikes over 15%, according to Mark Friedlander at the Insurance Information Institute. "We haven't seen these type of rates in quite a long time because the trend has been overall lower rate increases," Friedlander said. Higher costs to fix and replace homes and more severe weather losses have contributed to big increases last year in Florida. State leaders have also been pointing to a calmer insurance market since reforms were passed in December 2022 to cut down on fraudulent litigation. Friedlander said it doesn't seem likely the new rate hike requests will spread among other companies, which already had double-digit hikes in 2023. "The bottom line is, I don’t think it’s a trend that’s starting," Friedlander said. Original Article can be found here: 2 home insurance companies seek rate hikes over 50% (wptv.com) Although this is never what we want to see, at Anderson Agency Insurance, our goal is to keep you informed of what is going on in the insurance industry so that you can make informed decisions and stay ahead of the potential problems. If you would like us to look into a new policy or shop and existing one for you, click the button below.

Comprehensive auto insurance offers a wide-ranging level of protection for your vehicle, covering damages that occur outside of collisions. While liability insurance covers damages to other people's property or injuries they sustain in an accident where you are at fault, comprehensive insurance steps in to protect your own vehicle from a variety of non-collision-related risks.

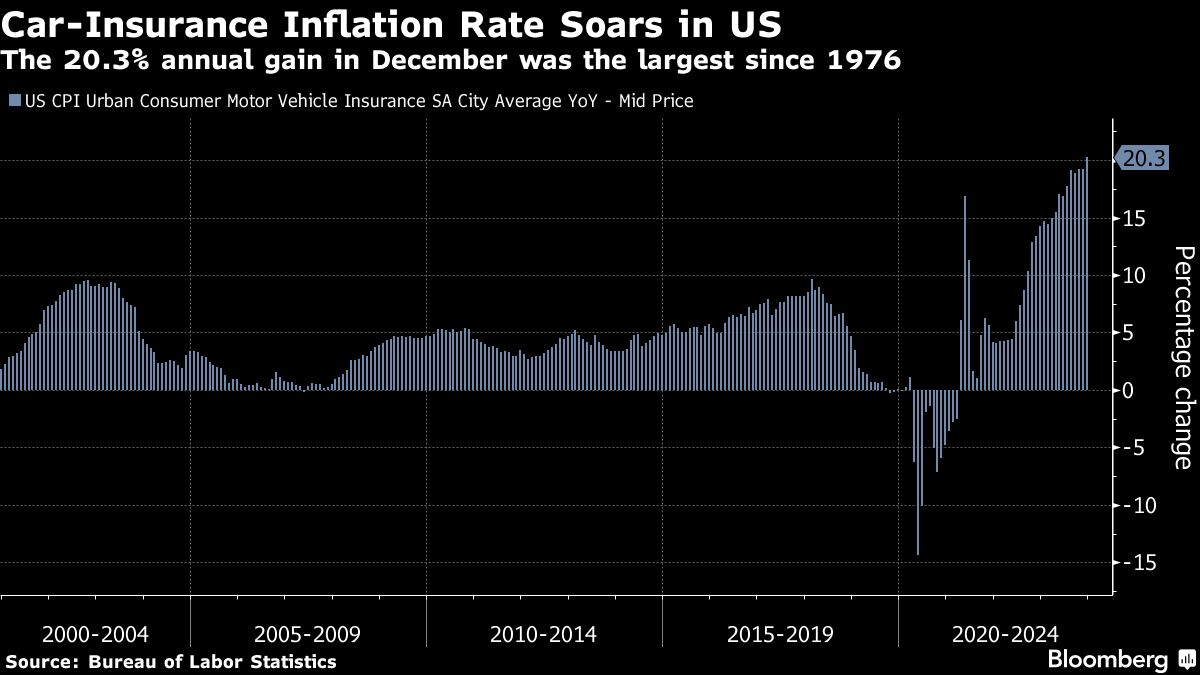

One of the primary benefits of comprehensive coverage is its protection against theft. If your car is stolen, comprehensive insurance can help cover the cost of replacing it, providing valuable financial support during a stressful time. This coverage extends beyond theft to include vandalism, such as if your car is intentionally damaged by graffiti or broken windows. Natural disasters can wreak havoc on vehicles, but comprehensive insurance can provide a safety net in these situations. Whether it's damage from a hailstorm, flooding, or a falling tree branch, this type of coverage can help cover the cost of repairs or even the replacement of your vehicle if it's deemed a total loss. Additionally, comprehensive insurance covers damage caused by animals, such as hitting a deer or having your car scratched by a stray cat. These incidents may seem minor, but they can still result in costly repairs that comprehensive insurance can help mitigate. While comprehensive coverage is not legally required like liability insurance, it's often recommended for drivers who want to protect their investment in their vehicles. By providing coverage for a wide range of risks beyond collisions, comprehensive auto insurance offers valuable peace of mind and financial security for drivers facing unexpected challenges on the road. Interested in learning more, click the button below to get in contact with a member of our team!  There’s no relief in sight for US car owners who’ve faced soaring costs of maintaining a vehicle in the past two years. Prices of motor-vehicle insurance rose 20.3% in December from a year earlier, the biggest jump since 1976, according to the Bureau of Labor Statistics. That was the 16th straight month of annual gains exceeding 10%. And insurance rates will probably keep on rising, propelled by higher costs of replacement parts and repairs, Bloomberg Intelligence analysts said last month. Prices of used cars and trucks have come down from their peaks two years ago. But the December consumer-price index released Thursday showed an uptick in used-vehicle costs from the previous month, defying economists forecasts for a decline. The surprise monthly increase in that category was among the main drivers of a acceleration in the overall rate of inflation. Even after a drop in 2023, used-vehicle prices remain up 38% since the start of the pandemic. As for new cars and trucks, prices are not increasing nearly as much as they did in 2022. On an annual basis, they were up only 1% in December. Photo: Photographer: Kyle Grillot/Bloomberg Article shared from Insurance Journal - Original Article can be found here: Auto Insurance Costs Soar by 20% in the US (insurancejournal.com) At Anderson Agency Insurance we recognize how discouraging and frustrating it is that rates continue to rise. Our goal is to provide the best customer service by finding the best policy for YOUR needs. We are on your side.

Click below to allow us the opportunity to review your current policy to see if there is anything we can do to help, or to allow us to shop a new policy for you!  Every year there are a few items that you must ensure are checked off of the to-do list! Here are a few things that everyone needs to check into to make sure they are up-to-date and fully protected. Things change year to year, from health to financial situations and we want to make sure you go into this new year more prepared! 1. Schedule your annual physical. 2. Schedule your annual eye appointment. 3. Schedule a dentist appointment. 4. Replace the smoke detector in your home. 5. Have your tires checked and rotated. 6. Schedule a vet appointment for your pet. 7. Begin organizing your tax documents for annual tax filing. 8. Schedule an appraisal appointment for your new holiday jewelry or family heirlooms. 9. Estate Plan in place and up to date. 10. CHECK YOUR INSURANCE POLICIES TO ENSURE THEY ARE UP-TO-DATE and CORRECT. Have a policy that you need to have reviewed or in need of a new insurance policy quote? We can help! Click the button below to submit your request!

|

Anderson Agency of Northeast Florida in Ponte Vedra, provides great products at competitive pricing and can help with all of your insurance needs including: Homeowner's Insurance, Auto Insurance, Umbrella Insurance, Renter's Insurance, Boat Insurance, and Jet Skis, Travel Trailers, and RV Insurance. Anderson Agency serves Jacksonville. Ponte Vedra Beach, Jacksonville Beach, Atlantic Beach, Neptune Beach, Nocatee & St. Johns, Florida.

We are your go-to , trusted Ponte Vedra Insurance agency!

For more information call 904-834-8088 or email us at info@AndersonAgencyfl.com

Located:

820 A1a North

Ste W11,

Ponte Vedra Beach, FL 32082

We are your go-to , trusted Ponte Vedra Insurance agency!

For more information call 904-834-8088 or email us at info@AndersonAgencyfl.com

Located:

820 A1a North

Ste W11,

Ponte Vedra Beach, FL 32082